AG Report Finds New Yorkers of Color Are Far Less Likely to Own a Home, More Likely to Be Denied Mortgages, and Face Higher Borrowing CostsDisparities Cost Black and Latino Borrowers More Than $200 Million over the Course of Their MortgagesNew York Attorney General Letitia James released a new report today detailing deep racial disparities in homeownership and access to home financing across the state. Among the report’s top findings is a stark racial gap in homeownership rates in every region in New York, with white households owning their homes at nearly double the rate of households of color. These disparities are a significant contributor to the racial wealth gap and result in higher housing costs for homebuyers of color, making it harder for communities of color to build lasting financial security and overcome decades of systemic discrimination in the housing market. The report also offers policy proposals to help close the homeownership gap.

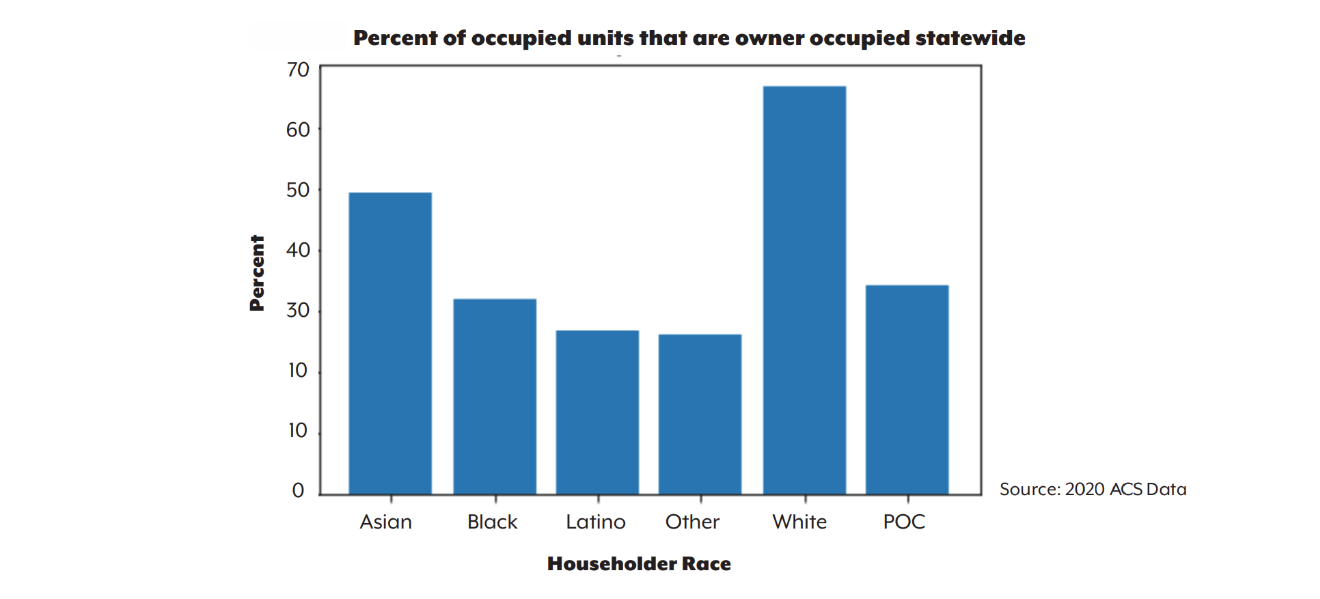

“Owning a home is an essential part of achieving the American dream and building wealth to pass on to future generations,” said Attorney General James. “Unfortunately, unequal access to affordable credit is still pervasive across our state, reinforcing the legacy of segregation, leading to a disparity in homeownership, and fueling the racial wealth gap. This report makes it clear that our state must do more to provide better resources for homebuyers and strengthen housing laws to help empower more New Yorkers. My office remains committed to fighting housing discrimination in all forms, and I look forward to working with my partners in government to address this problem.”The Office of the Attorney General's (OAG) report found that homeownership in New York is concentrated in white households and neighborhoods. This trend of lower homeownership rates for people of color is present throughout the state. The report noted that the city of Albany, the state’s capital, has the second-largest gap between white and Black homeownership of any city nationwide, second only to Minneapolis. Across New York, white households are 25 percent more likely than Asian households to own their home and more than twice as likely as Black or Latino households to own their home.

The report shows white households in New York are more than

twice as likely as Black or Latino households to own their home

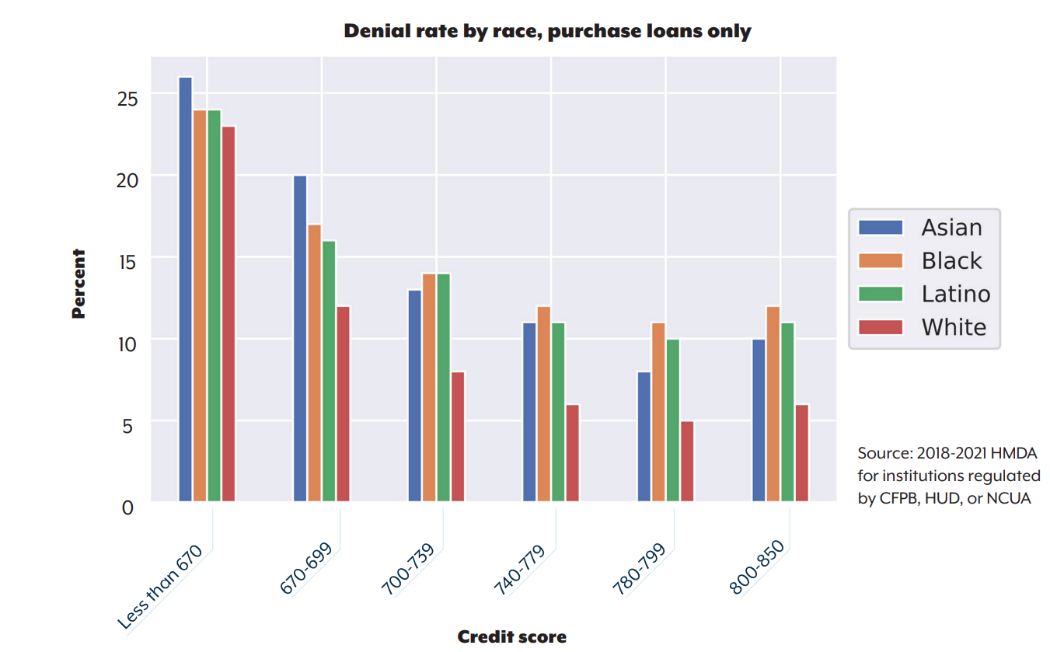

The report also reveals the significant barriers that borrowers of color face when attempting to purchase a home. Not only are Black and Latino New Yorkers disproportionately underrepresented among mortgage applicants, all applicants of color are denied mortgages at higher rates than white applicants, regardless of credit score, income, size of the loan, and other factors. Even among borrowers with the highest credit scores, non-white mortgage applicants are denied a mortgage at nearly double the rate of white applicants.

Across every credit score range, mortgage applicants

Across every credit score range, mortgage applicants

of color are denied at higher rates than white applicantsIn addition, OAG’s report revealed that non-white prospective homebuyers face higher costs than their white counterparts. They are more likely to be charged higher interest rates for their loans, more likely to use costlier Federal Housing Administration loans, and less likely to be approved to refinance their loans to a lower rate. These added burdens total over $200 million more in interest and other costs over the course of Black and Latino borrowers’ loans.

The report identifies a number of state-level policy solutions that could help close the racial homeownership gap, including:

- Subsidizing down payments and interest rates for first-generation home buyers — who are disproportionately people of color — to make it easier for families who have never bought a home to get credit.

- Increasing state funding to nonprofit financial institutions that can better support communities of color underserved by traditional financial institutions.

- Passing the New York Public Banking Act to create a regulatory framework for cities, towns, and regions to establish public banks. These institutions would help expand access to affordable financial services in underserved communities.

- Increasing resources for government agencies' fair lending investigations and strengthening New York’s Human Rights Law to expressly prohibit lending practices that have a disparate impact on communities of color.

- Exploring options for state-provided banking services at places like libraries and post offices to help reduce the population of New Yorkers who lack adequate access to traditional banking services.

The OAG’s report was prepared by Jasmine McAllister, Gautam Sisodia, and Blake Rubey of OAG’s Research and Analytics Department, Megan Thorsfeldt and Jonathan Werberg formerly of the Research and Analytics Department, Mark Ladov of the Consumer Frauds Bureau, and Lindsay McKenzie and Joel Marrero of the Civil Rights Bureau. The Consumer Frauds Bureau is a part of the Division for Economic Justice, which is led by Chief Deputy Attorney General Chris D’Angelo. The Civil Rights Bureau is a part of the Division for Social Justice, which is led by Chief Deputy Attorney General Meghan Faux. Both the Division for Economic Justice and the Division for Social Justice are overseen by First Deputy Attorney General Jennifer Levy.

The Office of the Attorney General's (OAG) report found that homeownership in New York is concentrated in white households and neighborhoods. This trend of lower homeownership rates for people of color is present throughout the state. The report noted that the city of Albany, the state’s capital, has the second-largest gap between white and Black homeownership of any city nationwide, second only to Minneapolis. Across New York, white households are 25 percent more likely than Asian households to own their home and more than twice as likely as Black or Latino households to own their home.

The report shows white households in New York are more than

twice as likely as Black or Latino households to own their home

The report also reveals the significant barriers that borrowers of color face when attempting to purchase a home. Not only are Black and Latino New Yorkers disproportionately underrepresented among mortgage applicants, all applicants of color are denied mortgages at higher rates than white applicants, regardless of credit score, income, size of the loan, and other factors. Even among borrowers with the highest credit scores, non-white mortgage applicants are denied a mortgage at nearly double the rate of white applicants.

of color are denied at higher rates than white applicants

In addition, OAG’s report revealed that non-white prospective homebuyers face higher costs than their white counterparts. They are more likely to be charged higher interest rates for their loans, more likely to use costlier Federal Housing Administration loans, and less likely to be approved to refinance their loans to a lower rate. These added burdens total over $200 million more in interest and other costs over the course of Black and Latino borrowers’ loans.

The report identifies a number of state-level policy solutions that could help close the racial homeownership gap, including:

- Subsidizing down payments and interest rates for first-generation home buyers — who are disproportionately people of color — to make it easier for families who have never bought a home to get credit.

- Increasing state funding to nonprofit financial institutions that can better support communities of color underserved by traditional financial institutions.

- Passing the New York Public Banking Act to create a regulatory framework for cities, towns, and regions to establish public banks. These institutions would help expand access to affordable financial services in underserved communities.

- Increasing resources for government agencies' fair lending investigations and strengthening New York’s Human Rights Law to expressly prohibit lending practices that have a disparate impact on communities of color.

- Exploring options for state-provided banking services at places like libraries and post offices to help reduce the population of New Yorkers who lack adequate access to traditional banking services.

No comments:

Post a Comment